America's Trusted Land Buyers

Call Us Now at 469-599-2351

Surplus Funds Recovery

Home » Surplus Funds Recovery

What Are Surplus Funds?

When a property is sold at a foreclosure or tax sale, it often sells for more than what was owed. The extra money left over after paying off the debt is called surplus funds. By law, those funds belong to the former owner or their heirs — not the county, the lender, or the trustee.

Unfortunately, many families never claim this money because they don’t know it exists, or the process feels too complicated. That’s where we step in.

How ONE22 Investments Can Help

At ONE22 Investments, our primary business is real estate solutions. But over the years, we’ve seen too many families walk away from auctions unaware that money was left behind. That’s why we offer Surplus Funds Recovery Services.

We work closely with experienced attorneys who file claims directly with the trustee or court, ensuring the process is handled properly from start to finish. And here’s the best part — there are no upfront fees. We only succeed when you do.

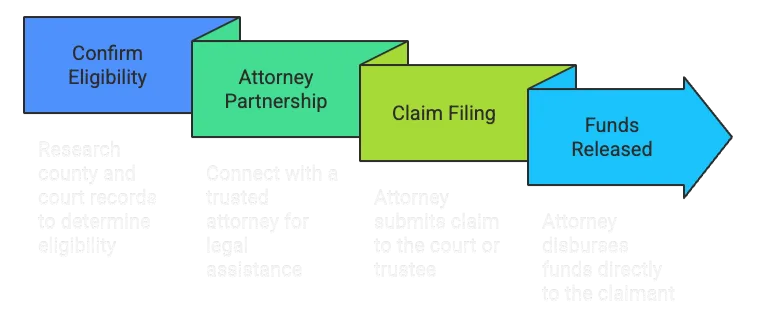

Our Process Is Simple

It’s that straightforward — no stress, no confusion, and no wasted time.

Why Work With ONE22 Investments?

Frequently Asked Questions

Am I really entitled to these funds?

Yes. If surplus funds exist after a foreclosure or tax sale, the previous homeowner or their heirs are legally entitled to claim them.

How long does the process take?

It depends on the county and court timelines, but most cases are resolved within a few months.

Do I have to live in Georgia to claim funds?

No — we can assist even if you live out of state.

Do I need to pay anything upfront?

No. We only collect a fee after your funds have been successfully recovered.

Take the Next Step

Don’t leave money unclaimed. If your property was recently sold at a foreclosure or tax sale, you may have surplus funds waiting for you.

📞 Call us today at 770-599-5723

📩 Or submit the quick form below to find out if you qualify